SE: under-appreciated recovery story?

plz let me know where i am wrong

*FYI, I am out of the L/S equity world (living the good life in credit) so I no longer have direct access to alt data. Alt data that I do have comes from friends so take it with a grain of salt.

It has been two years since my first SE post. With the stock down (65%) since my post, it is suffice to say it was prescient (unlike some of my other calls with a certain Dutch food delivery company) with a lot of my concerns coming to bear, especially with GMV growth rapidly normalising. In hindsight it was funny how some of the bulls (i.e. Mr Hong) were so confident in their top-down forecasts, implicitly forecasting 2022 net GMV additions to be greater than 2021 despite tough covid comps, reopening headwinds, macro headwinds, and reduced market share opportunity. Wished I kept the receipt before he nuked his account.

With that victory lap, I actually think SE is now an incredible opportunity and I would love to get feedback from the investment community that disagrees. I think SE is at a point of inflection and 2024 will be the year where GMV growth reaccelerates, profitability will improve meaningfully, and the bear case around TikTok Shop will be resolved, and you get to buy this business that can grow its normalized EBITDA at a 15%+ rate for what I believe to be a MSD NTM normalized EBITDA multiple (assuming shopee eventually gets to 2-3% ebitda % gmv margin). We might end 2024/2025 with investors eating out of Forrest Li hands again.

Shopee: GMV growth inflecting. EBITDA margin improving. TikTok competitive threat narrative to fade in 2024.

I think a lot of investors look at numbers and then find a convenient narrative that fits those numbers. One of the biggest bear narrative is that Shopee can’t grow and be profitable at the same time. This can be seen with the numbers - 1H EBITDA inflect positive but GMV growth collapsed, and 2H GMV growth inflected but EBITDA collapsed. GMV and EBITDA moves in opposite direction. As such the company can’t grow profitably and most of its orders must be zero-calories. While I do think there is some credence to this narrative, I believe it to be overhyped. 1H GMV decline was indeed due to the company shifting its focus to growth and pulled a bunch of promos and rebates and sales and marketing dollars, but these were orders that would have to been burnt off at some point anyway. They just did it all at once. GMV growth would have inflected positive anyway in the 2H once the company lap tough comps and went towards normalized level. Based on my estimate, core ecommerce (excluding livestreaming GMV) had already inflected to >10% YoY in 4Q despite the company continuously increasing take rate on the core eCommerce platform (and likely some cannibalization from the livestreaming business)

The reason why the company EBITDA went down was because the company is making the right strategic decision to expand into livestreaming with the company now growing a livestreaming platform that rivals TikTok Shop in 2 quarters

There is also evidence that Shopee Livestreaming losses have stabilised with my estimate of 4Q losses stable relative to 3Q level, with management hinting towards a trend towards breakeven for overall shopee in 2024 which implies Shopee Livestreaming losses improving sequentially over 2024.

I believe there is also evidence that TikTok Shop market share gain against Shopee has stabilized and has actually lost share to overall Shopee over the last few months. This makes sense to me as there is strong evidence that TikTok has largely captured its right-to-win portion of the market (discovery based fashion, beauty, and home & living) and incremental market share will be difficult to capture, especially with Shopee Livestreaming as a credible #2.

Lastly, I believe that TikTok acquiring Tokopedia is a good thing not a bad thing because it consolidated the market from 4 player to 3 player, and take out a desperate player that competes with 100% of Shopee GMV with a logical player that competes with 30% of Shopee GMV.

So this is what I think will happen to SE over 2024. Shopee GMV will inflect to 25%+ in 4Q23 and then sustains about 20% throughout 2024. Shopee EBITDA losses peak in 3Q23 and improve in 4Q23 and continue to improve sequentially over the next few quarters and breakeven sometime in 2H. Data will slowly come out that Shopee has fairly stable share against TT Shop and the narrative that they are not direct competitors will become the dominant narrative. Investors will then be able to start hallucinating about Shopee’s EBITDA potential again and the stock rips.

Garena and SeaMoney: Garena stable to improving. SeaMoney underappreciated.

I have limited differentiated insights when it comes to Garena but data has been positive and inflecting up so that is good. It seems to be that this asset should be worth $6B to $10B once EBITDA stabilises. I think it has.

SeaMoney looks underappreciated as well with most investors ignoring it right now. But once Shopee GMV growth and EBITDA starts to move the right direction, I think investors will look at this division and realize that there is a business that grew revenue at 37% in 3Q that is generating >$600 million of run-rate EBITDA. The SeaMoney business is closely tied to the Shopee business so as Shopee GMV inflects, so should SeaMoney.

So how much is all of this worth?

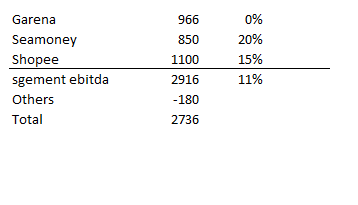

Using Visible Alpha consensus, Garena and SeaMoney should do $966 million and $850 million of EBITDA respectively and there is about $180 million of corporate costs and other stuff. This implies the company is able to generate $1.6 billion of EBITDA even without Shopee. I am inclined to believe Garena numbers are too high and SeaMoney numbers are too low.

How much EBITDA can Shopee generate in 2025? Let’s say it is 1% of GMV, that is $1.1B of EBITDA. This implies that SE can do $2.7B of EBITDA in 2025. And there is a lot of room for EBITDA margin to go when compared to global averages.

What should this business be worth? Blended EBITDA growth in 2025 should be at least 10% with upside if Shopee EBITDA margin improves. So maybe 20x EBITDA? Coupang trades around 20x EBITDA with low-teens revenue growth and also has a lot of room for margin to improve. Coupang is a lot more capital intensive but Shopee has a tougher competitive narrative and got to own Garena (yuck).

So that gets me to a stock at $54B which is about a double from here.

And there is probably more room for EBITDA to improve. Good luck and please DM me on twitter to let me know where I am wrong before I sling $100K more into this.

interesting data and comments from a peer https://x.com/portseacapital/status/1758226646971121676?s=20