[Special situation] Global Blue warrants - Asymmetric risk/reward

The subject of this post is something that falls out of what I believe is my circle of competence (food delivery, food tech, related industries). However, this idea looks really interesting and I would like feedback from the investment community. Am I missing something?

The opportunity

The idea is to long Global Blue August 2025 $11.50 strike call options. I have a position bought at around $1.25. I think the stock is mispriced and the warrants are mispriced relative to the stock. The warrants have a 5x potential from here, but could also be worthless (although that seems unlikely). So the reward to risk ratio is at least 5 to 1.

Based on my estimates, we are expecting a bulk of the returns to be extremely front loaded. We might get our 5x very quickly once international travel resumes, maybe by the end of 2021.

This return potential is possible because we are buying a levered instrument (warrants) on a levered company, with a lot of operating leverage, that is sensitive to international travel. It’s leverage on leverage on leverage to a macro situation that is extremely uncertain. So the risk is very high as well - this could be a $0 but i think there is a lot of time for this to work (warrant expires in 2025).

This is a PA idea because volume here is thin. The volume for $GB the equity is thin, and it’s even thinner for the warrants. The warrants trade $10k on a good day and the spread is wide.

The company

$GB is the largest VAT refund processor globally with 70% market share, 3x larger than the next largest competitor.

The company sits between merchants (such as Prada or Hermes) and the refund agents at the airport ($GB takes 15% from the VAT).

For investors familiar with other payment companies, this is similar to assets like Fleetcor and Edenred. It is an integrated network for a niche market segment.

The company also has a pretty good shareholder list.

$GB benefits from multiple secular growth drivers which should support over a decade of growth. More specifically, $GB benefits from the growth of international travel, especially from emerging markets like China.

This exposure to international travel also resulted in the demise of the asset in 2020 which resulted in a 95% decline in $GB revenue.

Impact and actions

The impact to revenue had a dramatic impact on profits as this is a high fixed cost business, and the business swung into losses. To make things worse, $GB also had a lot of debt.

The business was in peril, at least until it merged with a SPAC, Far Point Acquisition Corp, that gave it the necessary liquidity to survive.

To further starve off the risk of bankruptcy, $GB took actions to reduce fixed costs. Covid is the best time to implement ZBB.

It seems like the company now has enough liquidity to last through end 2022, assuming demand continues to be low at the current level.

I believe cash burn will be brought down to zero once regional borders reopen and demand returns >35% of 2019 level. The company won’t be profitable, but the risk of bankruptcy goes way down. Then, it just becomes a question of when and not if.

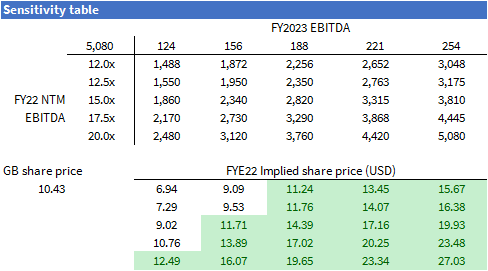

Earnings and share value

If $GB returns to pre-covid revenue level, it could generate €221mn of EBITDA.

This seems very possible. There is in fact a chance that demand will be much higher due to pent up demand. I believe this is called revenge spending.

Applying a range of possible outcomes suggests that there is quite a bit of upside here for the stock so long as we believe demand will return to a level anywhere close to 2019 level. This looks attractive in a world where every recovery stock is priced as if full recovery is a forgone conclusion.

Warrants

There is an even better way to invest in this idea and that is through the warrants (remember that Global Blue went public via a SPAC). It gives magnified equity upside, with lower downside risk and is more capital efficiency.

The downside is that there is a redemption feature which gives the company the right to redeem the warrants when the stock passes $18. I don’t think this means it will be put back at $18, but rather it can only be put back if it goes above $18. Either way, I assume the max return here is $18.

The risk reward for the warrants looks attractive at this price.

So how do we lose?

The risk here is that travel does not recover fast enough, especially because $GB is really dependent on Europe. But it seems we have a lot of time for this to work, and leading indicators such as Google Trends for Hotel Bookings and vaccination rate suggest we are coming back.

As always, please contact me if you think I am missing something. This is outside my circle of competence and so could easily miss something.

Other special situation posts

Why are the GB warrants trading for a third of the price of OSW's warrants? both SPACs, both travel related and badly hit by covid, both exposed to an $18 takeout and both underlying equity around the $10 mark.